Introductory Context

"A detailed guide to how mutual funds are classified based on structure, including open-ended, close-ended and interval schemes, with analysis of liquidity, risk and investor suitability."

Classification of Mutual Funds by Structure

Before discussing equity, debt or hybrid strategies, it is essential to understand how mutual funds are structurally designed. Structure determines how and when investors can enter or exit a scheme. It influences liquidity, portfolio management flexibility, redemption pressure and even the types of securities a fund manager can hold.

Two funds may both invest in equities, yet behave very differently if one is open-ended and the other is close-ended. Structure therefore affects operational dynamics as much as investment strategy.

In India, mutual fund schemes are structurally classified into three types:

Open-Ended Schemes

Close-Ended Schemes

Interval Schemes

Let us examine each in depth.

1. Open-Ended Schemes

An open-ended mutual fund scheme allows investors to buy and redeem units on any business day at the prevailing Net Asset Value (NAV), subject to cut-off timing rules.

There is no fixed maturity date. The scheme continues indefinitely unless wound up under regulatory procedures.

This structure is the most common and widely used format in India.

How It Works

When an investor purchases units:

New units are created and allotted.

When an investor redeems units:

Units are extinguished.

Money is paid out from the scheme’s portfolio.

Because units are continuously created and cancelled, the fund size expands and contracts dynamically.

Liquidity Characteristics

Open-ended schemes offer high liquidity. Investors do not need to wait for maturity or depend on stock exchange buyers.

However, this liquidity creates operational pressure on the fund manager. The portfolio must maintain adequate liquid assets to meet redemption requests.

During market stress, heavy redemptions can force selling of securities.

Advantages of Open-Ended Structure

Continuous entry and exit

Daily NAV transparency

Suitable for SIP-based investing

Ideal for goal-based accumulation

Ideal for SIP Investors

Open-ended schemes are structurally suited for systematic investment plans due to continuous subscription availability.

Risks and Limitations

The flexibility of open-ended funds also introduces challenges:

Redemption pressure during market panic

Need to maintain liquidity buffers

Portfolio adjustments due to cash flows

While structure does not change market risk, it changes liquidity risk dynamics.

2. Close-Ended Schemes

A close-ended scheme has a predefined maturity period — for example, 3 years or 5 years. Investors can subscribe only during the New Fund Offer (NFO) period.

After the NFO closes:

No fresh units are issued.

Redemption is not allowed until maturity.

Some close-ended schemes are listed on stock exchanges, allowing investors to sell units in the secondary market.

Portfolio Flexibility

Because redemption pressure is absent during tenure, close-ended schemes may invest in relatively less liquid securities.

For example:

Fixed Maturity Plans (FMPs) invest in debt instruments maturing in alignment with scheme tenure.

Certain capital protection-oriented schemes rely on fixed tenure structure.

Absence of daily redemption pressure gives fund managers stability in portfolio construction.

Liquidity Reality Check

While listed on exchanges, close-ended schemes often trade at a discount or premium to NAV depending on demand-supply dynamics.

Exchange liquidity may be limited.

Investors must therefore treat close-ended schemes as tenure-based commitments rather than daily tradable instruments.

Limited Liquidity Risk

Close-ended schemes may not provide easy liquidity despite stock exchange listing.

3. Interval Schemes

Interval schemes combine features of open-ended and close-ended structures.

They remain closed for transactions except during predefined intervals — for example, once every quarter.

During the interval window:

Investors may purchase or redeem units.

Outside the window, transactions are not permitted.

This structure attempts to balance liquidity access with portfolio stability.

Why Interval Structure Exists

Certain asset classes — especially structured credit or less liquid instruments — benefit from reduced redemption frequency. Interval schemes provide managers with predictable liquidity windows.

They are relatively less common compared to open-ended schemes.

Controlled Liquidity Model

Interval schemes provide liquidity only during predefined windows, reducing continuous redemption pressure.

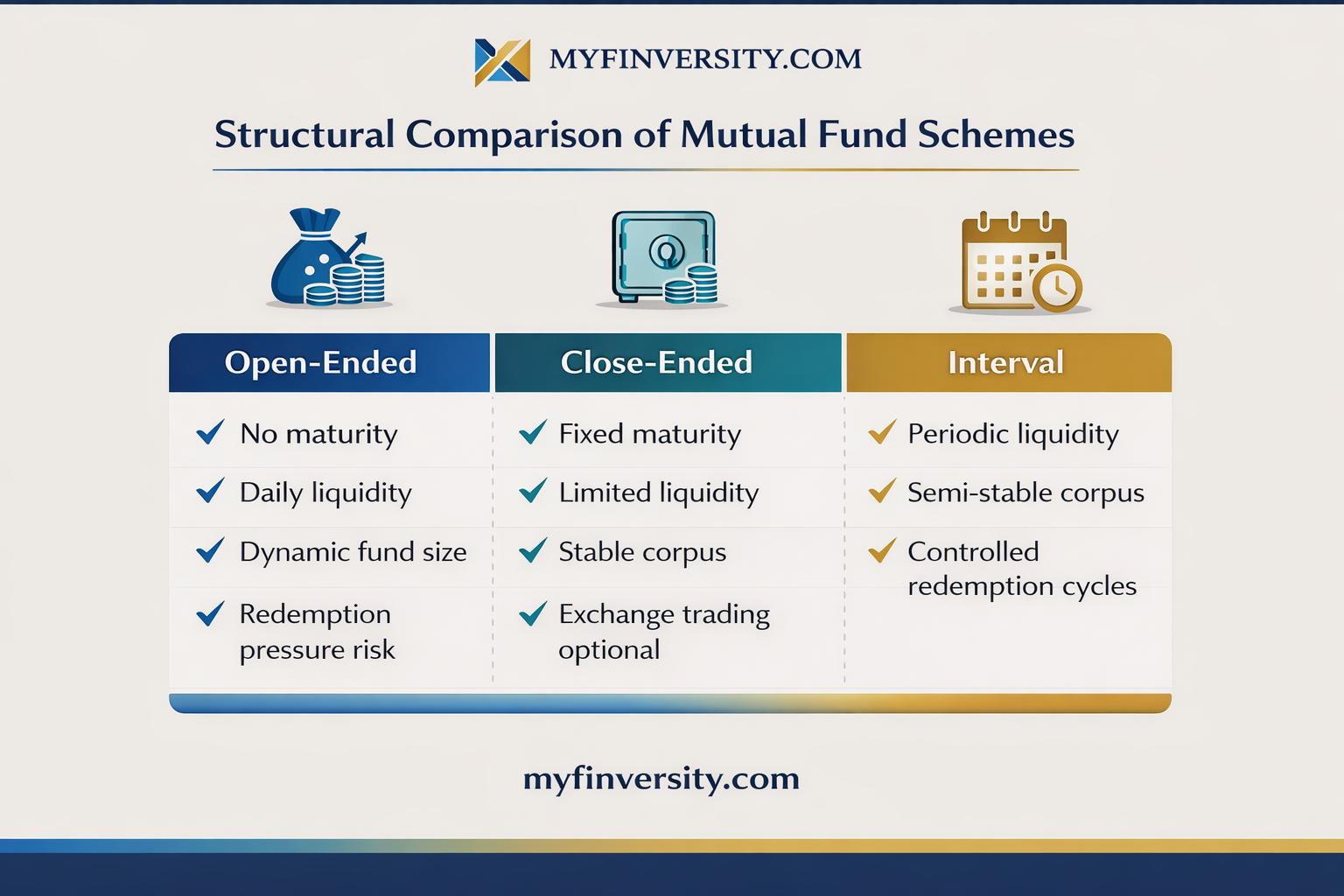

Structural Comparison Summary

Let us compare the three structures clearly:

Open-Ended

No maturity

Daily liquidity

Dynamic fund size

Redemption pressure risk

Close-Ended

Fixed maturity

Limited liquidity

Stable corpus

Exchange trading optional

Interval

Periodic liquidity

Semi-stable corpus

Controlled redemption cycles

How Structure Impacts Investment Strategy

Structure influences portfolio decisions:

Open-ended debt funds must manage daily liquidity carefully.

Close-ended debt funds can match asset maturity to scheme maturity.

Equity funds in open-ended format must manage volatility-induced redemptions.

Fund managers design portfolios differently depending on structure.

Structure therefore affects risk management strategy.

Structure Misunderstanding Risk

Investing in a close-ended scheme assuming daily liquidity can lead to liquidity disappointment.

Suitability Considerations

Investors must align structure with financial goals:

Short-term liquidity needs → Open-ended

Defined investment horizon → Close-ended

Semi-liquid strategic exposure → Interval

Structure should be evaluated before analyzing asset allocation.

Final Perspective

Structural classification is the foundation of product understanding. Before evaluating performance or expense ratio, investors must ask:

Is this scheme open-ended, close-ended or interval?

Structure determines liquidity, portfolio flexibility and investor access. While asset class determines risk-return profile, structure determines behavioral and operational characteristics.

Understanding this distinction prevents misaligned expectations.