Introductory Context

"A detailed explanation of how mutual funds are classified based on management style, covering active vs passive investing, index funds, ETFs, cost structures, tracking error and investor suitability."

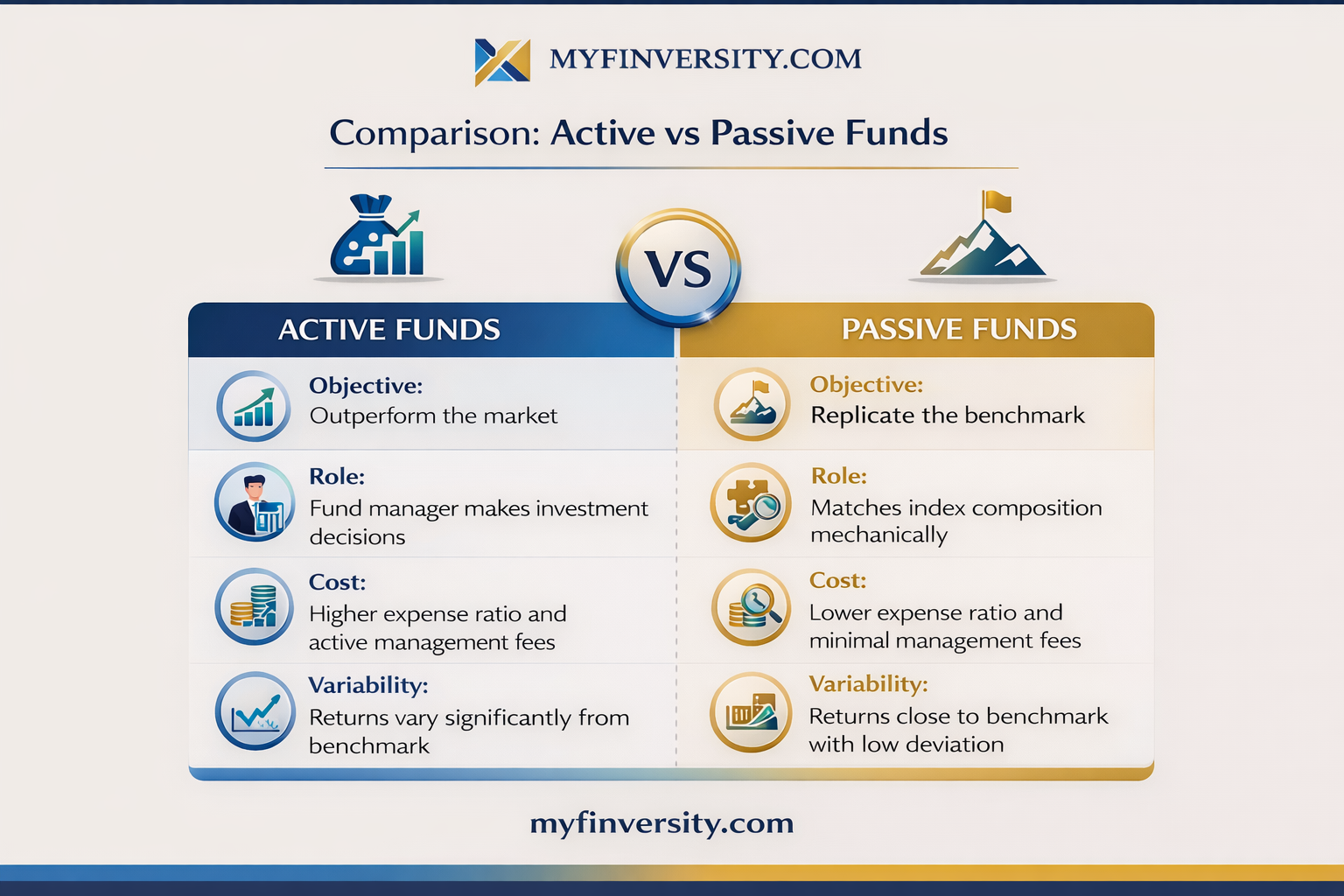

Classification of Mutual Funds by Management Style

Not all mutual funds are managed in the same way. Two equity funds may invest in the same market, yet their approach to stock selection, risk control, and performance measurement can differ fundamentally.

This difference arises from management style.

While structural classification determines liquidity and asset classification determines risk exposure, management style determines how returns are pursued. It defines whether a fund attempts to outperform the market or simply replicate it.

In India, mutual funds are broadly classified into:

Actively Managed Funds

Passively Managed Funds

Understanding this distinction is essential because it affects cost, performance expectation, volatility behavior, and long-term strategy.

I. Actively Managed Funds

An actively managed fund is one where a professional fund manager makes discretionary decisions about:

Which securities to buy

When to buy or sell

How much weight to allocate

Which sectors to overweight or underweight

The objective of active management is to generate alpha — that is, returns higher than the benchmark index.

For example, a large-cap equity fund may use Nifty 100 as its benchmark. An active fund manager will attempt to outperform this index through stock selection and timing decisions.

How Active Management Works

Active management relies on:

Fundamental research

Economic forecasting

Sector analysis

Company earnings projections

Valuation assessment

Risk management overlays

Portfolio composition may deviate significantly from the benchmark.

This deviation is often measured through metrics like active share and tracking difference.

Alpha Objective

Actively managed funds aim to outperform their benchmark index through research-driven security selection.

Cost Structure of Active Funds

Because active management requires research teams, analyst coverage, and portfolio turnover, expense ratios are generally higher compared to passive funds.

Costs include:

Fund management fees

Research expenses

Transaction costs

Portfolio churn impact

Higher cost does not guarantee higher returns. It only reflects a more intensive management process.

Cost vs Performance Reality

Higher expense ratios in active funds do not automatically translate into superior returns.

Strengths of Active Management

Active funds may offer:

Downside risk management in volatile markets

Tactical sector allocation

Ability to avoid weak stocks

Flexibility to hold cash (in certain strategies)

In inefficient markets or specific segments like small caps, active management may potentially add value.

Limitations of Active Management

However, active funds also face challenges:

Consistency of outperformance is difficult

Performance depends on fund manager skill

Style drift risk

Higher cost drag

Long-term alpha generation requires sustained skill — which is statistically challenging across large universes.

II. Passively Managed Funds

Passively managed funds do not attempt to outperform a benchmark. Instead, they aim to replicate the performance of a specified index.

Examples include:

Nifty 50 Index Funds

Sensex ETFs

Nifty Next 50 Index Funds

The fund manager does not make discretionary stock selection decisions beyond maintaining alignment with the benchmark.

How Passive Management Works

In passive funds:

Portfolio composition mirrors the benchmark index.

Weightage of each stock matches index allocation.

Rebalancing occurs when index constituents change.

Performance objective is not alpha generation but tracking accuracy.

The difference between fund return and benchmark return is called tracking error.

Tracking Error Defined

Tracking error measures how closely a passive fund replicates its benchmark performance.

Cost Advantage of Passive Funds

Because passive funds do not require extensive research or frequent trading, their expense ratios are typically lower.

Lower costs improve long-term compounding efficiency.

This cost advantage becomes significant over extended investment horizons.

Long-Term Cost Efficiency

Even small differences in expense ratio can significantly impact long-term returns due to compounding.

Index Funds vs ETFs

Within passive management, two common vehicles exist:

Index Funds

Purchased and redeemed directly with AMC

NAV-based pricing

Suitable for SIPs

No demat account required

Exchange Traded Funds (ETFs)

Listed and traded on stock exchanges

Bought and sold like stocks

Require demat and trading account

Price may vary slightly from NAV due to market demand

While both track indices, liquidity mechanics differ.

ETF Liquidity Risk

Low trading volume in ETFs may lead to price deviations from NAV in certain market conditions.

When Does Each Style Make Sense?

Active management may be suitable when:

Market inefficiencies exist

Fund manager track record is strong

Investor seeks tactical flexibility

Passive management may be suitable when:

Long-term compounding is priority

Cost efficiency matters

Broad market exposure is desired

Investor prefers simplicity

Both styles can coexist in a diversified portfolio.

Hybrid Approach in Modern Portfolios

Many investors combine active and passive funds. For example:

Passive large-cap exposure

Active mid-cap allocation

Passive international exposure

Management style is not a binary choice — it is a strategic allocation decision.

Final Perspective

Classification by management style clarifies the philosophy behind a mutual fund. Active funds attempt to outperform markets through skill and research. Passive funds accept market returns and optimize cost efficiency.

Neither approach is universally superior. Their effectiveness depends on:

Market conditions

Cost structures

Time horizon

Investor discipline

Understanding management style prevents unrealistic expectations and aligns strategy with financial goals.

In the next section, we move to classification by investment universe — where we examine how schemes are categorized based on asset allocation and investment mandate.