Detailed Introductory Concept

There are decisions in life that feel powerful the moment you make them. Choosing a career. Buying a home. Launching a business.

And then there are decisions that feel ordinary when you make them — but quietly shape the entire trajectory of your future.

Starting to invest early belongs to the second category.

When someone in their twenties delays investing, it rarely feels dangerous. Income is still rising. Responsibilities are manageable. Retirement is distant. Ten years seems like a small fraction of a lifetime.

But compounding does not evaluate time emotionally. It evaluates it mathematically.

The Early Start Advantage explains why two individuals with similar discipline, similar income, and similar returns can reach dramatically different financial outcomes simply because one began earlier. It is not a motivational principle. It is a structural reality embedded in exponential growth.

Time inside compounding systems does not behave passively. It multiplies.

The Calm Beginning That Hides Its Importance

In the first few years of investing, growth is rarely impressive. Monthly contributions accumulate slowly. Annual returns appear incremental. The increase in total wealth feels modest.

This visual calm creates a dangerous assumption: that the early years are flexible.

Because the curve appears shallow, people conclude that starting later will not matter much. The belief forms quietly — “I can begin seriously when my income increases.” Or “Once I’m more financially confident, I’ll start properly.”

What this belief ignores is that compounding builds structure before it builds scale.

Each year’s return becomes part of the capital that generates the next year’s return. That next return then becomes part of the base again. In the beginning, this layered growth is subtle. Over time, it becomes powerful.

The early years are not about dramatic gains. They are about establishing the base that later acceleration depends upon.

Remove the first decade, and the acceleration phase never reaches the same height.

Compounding Does Not Add — It Multiplies

Most people intuitively think in linear terms. If you save for ten more years, you expect ten more units of progress. If you invest twice as much, you expect roughly twice the result.

Compounding does not operate linearly. It operates exponentially.

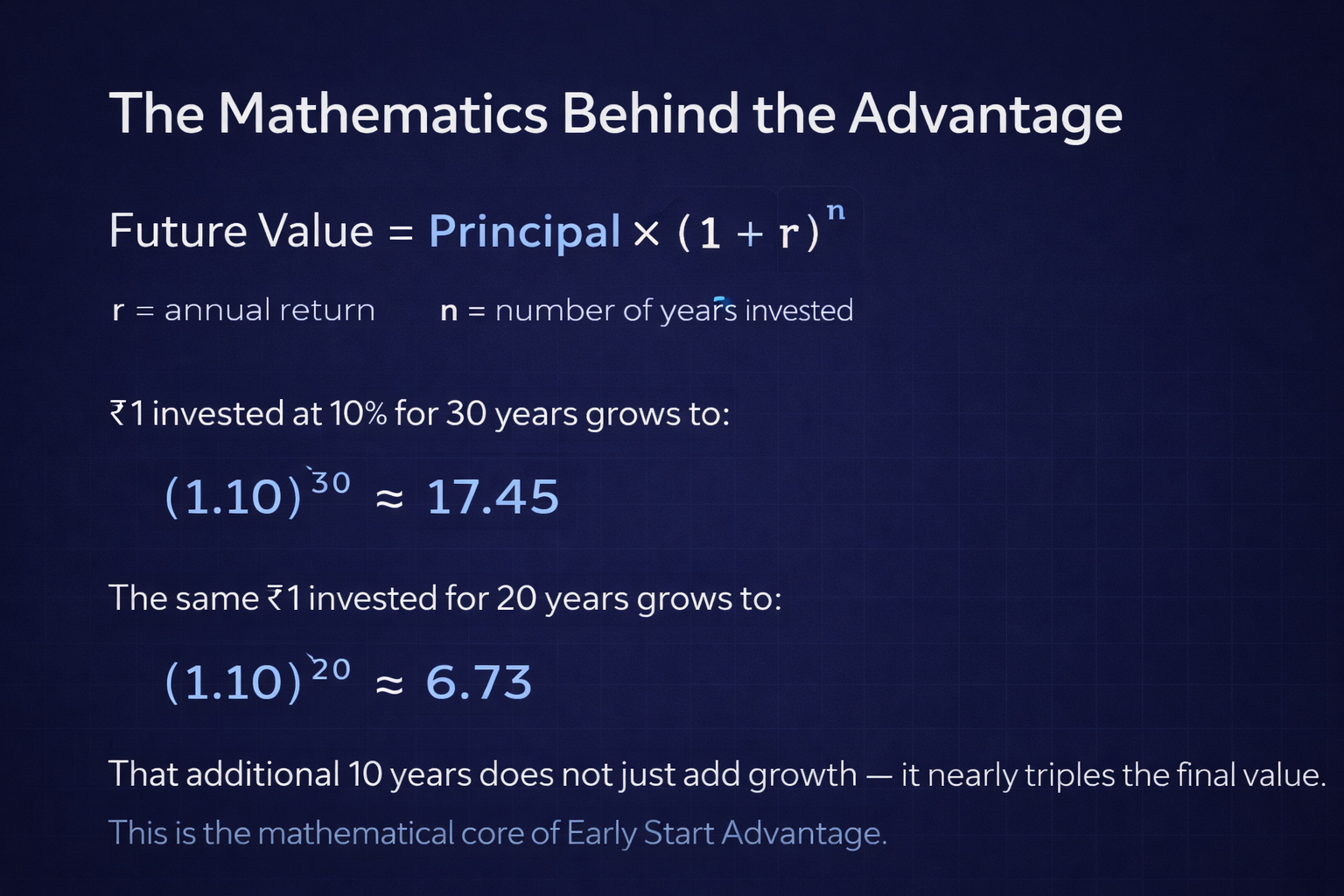

When returns are reinvested, growth feeds on prior growth. The structure can be represented mathematically as:

Future Value = Principal × (1 + r)ⁿ

The critical insight is that time sits in the exponent. When a variable is in the exponent, even small changes in it create disproportionately large changes in outcome.

An additional five or ten years of compounding does not simply add growth. It multiplies the accumulated base repeatedly.

This is the mathematical engine behind the Early Start Advantage.

Exponential Structure

In compounding systems, time sits in the exponent. Small differences in duration create large differences in final outcomes.

The Invisible Cost of Delay

When someone postpones investing by five or ten years, the cost does not feel immediate. There is no penalty notice. No visible loss appears on a statement.

But the cost exists in the form of missing multiplication cycles.

If an investor begins at twenty-five instead of thirty-five, the difference is not simply ten years of contributions. It is ten years of compounded growth layered upon itself. Those early cycles would have continued multiplying throughout the remaining investment horizon.

Remove them, and the ceiling lowers permanently.

The Early Start Advantage is not about urgency. It is about participation duration.

Why Larger Contributions Later Rarely Fully Catch Up

A common argument suggests that starting late can be offset by investing more aggressively later. While higher contributions certainly improve outcomes, they operate within a shortened compounding window.

Increasing the principal increases the base. Increasing time multiplies the entire structure repeatedly. These two adjustments are not equivalent.

An early investor benefits from growth on contributions and growth on previous compounded growth for a longer period. A late investor begins building that layered base much later, limiting total acceleration.

Money can be increased. Past time cannot.

Irreversibility

You can increase contributions later. You cannot recover lost compounding years.

Time as a Risk Buffer

Another dimension of the Early Start Advantage is resilience.

Markets fluctuate. Economic cycles shift. Returns are not smooth every year. An investor with a longer time horizon has more years available for recovery. Temporary downturns become smaller relative to total duration.

A late starter operates within a compressed timeline. A major downturn close to a financial goal can have amplified consequences because fewer recovery cycles remain.

Time provides not only growth but flexibility and recovery capacity.

Duration Builds Resilience

A longer investment horizon allows capital to absorb volatility and recover from downturns more effectively.

The Acceleration Phase Comes Later

One of the most misunderstood aspects of compounding is that most of the dramatic growth occurs in later years.

In the beginning, growth feels modest. In the middle years, it becomes noticeable. In the final phase, it accelerates rapidly.

That late acceleration is only possible because earlier years built a substantial base. Remove the early contributions, and the later acceleration phase weakens significantly.

The Early Start Advantage is not about early returns. It is about enabling later acceleration.

The Psychological Bias Against Early Action

Human beings naturally discount distant outcomes. A decade feels long when looking forward and short when looking backward. This bias makes delay feel harmless.

Compounding does not respond to perception. It responds to duration.

The early years feel flexible precisely because their importance is not immediately visible. By the time their value becomes clear, they are gone.

This is why the Early Start Advantage often goes unappreciated until later in life.

Psychological Illusion

The early phase of compounding feels slow. Its importance becomes visible only decades later.

Practical Implications

The Early Start Advantage explains why financial planners encourage starting with small, consistent investments rather than waiting for larger sums.

A modest contribution begun early often outperforms a larger contribution begun late because duration multiplies efficiency.

The size of the first step matters less than the timing of the first step.

Consistency begun early compounds quietly into scale.

Final Perspective

The Early Start Advantage is not about perfection or extraordinary returns. It is about entering the compounding system as early as possible and allowing time to perform its multiplication.

In exponential systems, duration dominates intensity.

The difference between starting at twenty-five and starting at thirty-five is not simply ten years of savings. It is ten multiplication cycles that will never occur again.

Income can increase. Contributions can rise. Strategy can improve.

Past time cannot be reinvested.

In the architecture of wealth creation, the moment you begin quietly determines how far you can ultimately go.

Frequently Asked Questions

Disclaimer: While due care has been taken to ensure the accuracy, clarity, and relevance of the information, the content is intended solely for educational purposes. Financial terms and concepts are interpretative tools; readers are strongly advised to verify information from multiple sources and apply their own judgment. This content does not constitute financial, investment, or advisory recommendations of any kind.