Introductory Context

"A deep and structured explanation of Growth and IDCW (Income Distribution cum Capital Withdrawal) options in mutual funds, including taxation, compounding impact, behavioural traps and long-term wealth implications."

Growth vs IDCW Option in Mutual Funds

Among all the choices investors make in mutual funds, few are as misunderstood as the choice between Growth and IDCW options.

Many investors believe IDCW provides “extra income.”

Some believe Growth is only for long-term investors.

Others assume dividend-paying funds generate better returns.

Most of these beliefs are partially incorrect.

To understand the difference properly, we must begin with one important principle:

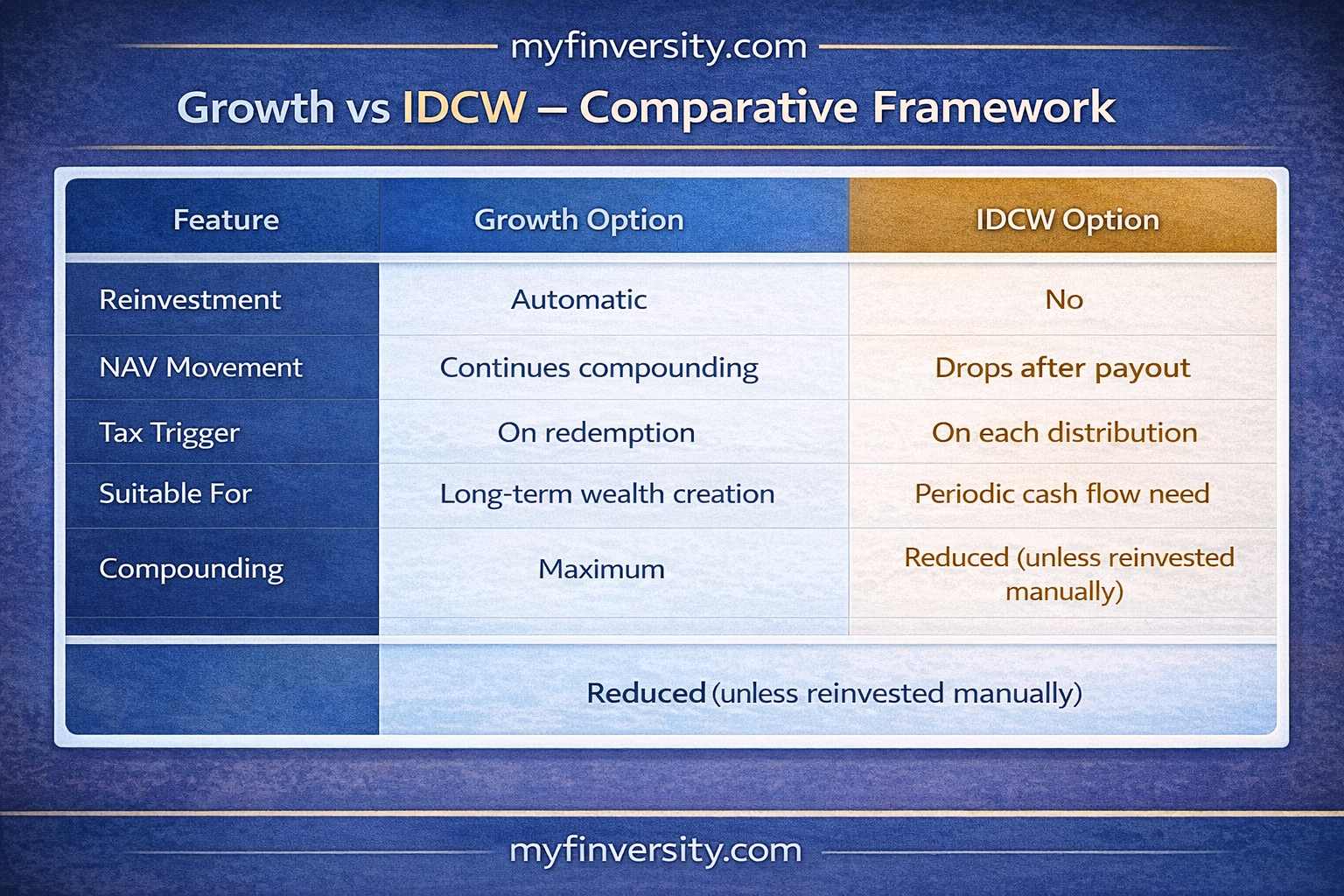

A mutual fund does not create two separate portfolios for Growth and IDCW options. The underlying investments are identical.

The difference lies in how gains are treated.

What Is the Growth Option?

In the Growth option, all profits earned by the mutual fund — whether from capital appreciation, interest income, or dividends received from underlying securities — are reinvested into the portfolio.

Nothing is paid out to investors.

As a result:

NAV keeps increasing over time (subject to market movement)

Gains compound within the fund

Investor wealth grows through reinvestment

The Growth option is designed for capital accumulation.

It maximises compounding.

What Is the IDCW Option?

IDCW stands for Income Distribution cum Capital Withdrawal.

Earlier, this was simply called “Dividend Option.” However, SEBI mandated the terminology change because the word “dividend” was misleading.

In the IDCW option:

The fund distributes a portion of accumulated gains to investors.

NAV falls to the extent of the payout.

The distributed amount may include both income and capital component.

This is critical.

The payout is not “extra return.” It is money taken out of your own investment pool.

Structural Reality

IDCW is not additional profit. It is distribution of gains from the same portfolio, reducing NAV accordingly.

Why SEBI Changed the Term from Dividend to IDCW

The word “dividend” in stocks refers to profit distribution from a company’s earnings.

But in mutual funds:

Distribution may include realized capital gains.

Distribution may include part of capital.

It is not necessarily pure income.

To prevent mis-selling and confusion, SEBI introduced the term IDCW in 2021 to clarify that payout may include capital withdrawal.

This regulatory change reflects how frequently investors misunderstood the concept.

How NAV Behaves in Growth vs IDCW

Let us understand through an example.

Suppose a fund has NAV of ₹20.

If the fund declares IDCW of ₹2 per unit:

₹2 is paid to investors.

NAV drops from ₹20 to ₹18.

Your total wealth remains the same immediately after distribution.

Earlier:

10 units × ₹20 = ₹200

After IDCW:

10 units × ₹18 = ₹180

Cash received = ₹20

Total = ₹200

Nothing magical happened.

Money moved from the fund to your bank account.

Common Misbelief

IDCW does not mean the fund is generating extra income. It is distributing part of your accumulated gains.

Compounding Impact – The Real Difference

Here lies the core distinction.

In the Growth option:

Gains remain invested.

Future returns are generated on a growing base.

Compounding accelerates over time.

In the IDCW option:

Gains are periodically removed.

Compounding base reduces.

Long-term corpus grows slower (unless reinvested manually).

Over long horizons, compounding makes a substantial difference.

This is why Growth option is generally preferred for long-term wealth creation.

Behavioural Dimension

Why then do many investors choose IDCW?

Two primary reasons:

Psychological comfort of “income”

Misunderstanding that dividend equals profit

Many retired investors believe IDCW generates steady income like interest from a fixed deposit.

However, unlike FD interest (which is contractual), IDCW payouts are:

Not guaranteed

Not fixed

Declared at fund house discretion

Dependent on available distributable surplus

This unpredictability makes IDCW unsuitable as a reliable income replacement unless structured carefully.

Taxation Difference

Tax treatment further differentiates Growth and IDCW.

In the Growth option:

Tax is triggered only when you redeem units.

Capital gains tax applies (short-term or long-term depending on holding period).

In the IDCW option:

Distribution is taxable in the hands of the investor as per applicable slab (as per current rules).

TDS may apply if distribution exceeds threshold limits.

Therefore, IDCW may create recurring tax events even without redemption.

For high tax bracket investors, this can reduce net returns significantly.

Tax Efficiency

Growth option is generally more tax-efficient for long-term investors due to deferred taxation.

When IDCW May Be Appropriate

Despite limitations, IDCW may be suitable in certain situations:

Retirees seeking periodic cash flow

Investors consciously using distribution for planned expenses

Situations where reinvestment discipline is weak

However, even in retirement, systematic withdrawal plans (SWP) from Growth option often provide better control and tax efficiency.

Analytical Perspective

Over 15–20 years, even small periodic distributions can significantly reduce final corpus due to interrupted compounding.

The Growth option allows time to work uninterrupted.

IDCW interrupts time’s compounding power.

The choice therefore is not about “income vs growth.”

It is about:

Immediate cash flow

versus

Maximum long-term capital expansion

Decision Framework

Ask yourself:

Do I need regular income right now?

Am I in a high tax bracket?

Am I investing for long-term wealth accumulation?

Do I understand that IDCW reduces NAV?

If the goal is wealth creation → Growth is generally superior.

If the goal is structured income → Evaluate IDCW vs SWP carefully.

Final Perspective

Growth and IDCW are not two different investment strategies. They are two different payout mechanisms applied to the same portfolio.

One maximises compounding.

The other distributes gains periodically.

Clarity on this concept prevents one of the most common retail investing mistakes in India — chasing dividend payouts under the illusion of higher returns.

Understanding this distinction strengthens long-term decision-making discipline.