Introductory Context

"A complete explanation of the difference between Direct and Regular mutual fund plans, including expense ratio impact, distributor commissions, NAV differences and long-term return implications."

Direct vs Regular Plans in Mutual Funds

At first glance, Direct and Regular plans of a mutual fund appear identical. They invest in the same portfolio, are managed by the same fund manager, follow the same strategy, and declare NAV daily. Yet over time, the difference between them can significantly impact long-term wealth.

Understanding this distinction is essential, especially for investors who intend to build wealth through disciplined compounding over many years.

The difference between Direct and Regular plans lies not in the investment strategy but in the distribution model and cost structure.

Why Two Plans Exist

Mutual fund houses offer two versions of most schemes:

Direct Plan

Regular Plan

Both invest in the same underlying securities. However, the route through which the investor invests determines which plan applies.

When an investor invests directly through the fund house website or certain platforms without distributor involvement, the Direct Plan is applicable.

When an investor invests through an intermediary such as a distributor, broker, or advisor who earns commission, the Regular Plan is applicable.

The difference is therefore structural — not strategic.

Key Structural Difference

Direct Plans exclude distributor commissions. Regular Plans include them.

Expense Ratio: The Real Difference

The most important practical difference between Direct and Regular plans is the expense ratio.

Because Regular plans include commission paid to distributors, their expense ratio is slightly higher than that of Direct plans.

The additional cost may appear small — often between 0.5% to 1% depending on category — but compounding amplifies this difference over time.

Suppose two identical schemes deliver 12% gross annual return before expenses.

If:

Direct Plan expense ratio = 1%

Regular Plan expense ratio = 2%

The net returns will differ by 1% annually.

Over 15–20 years, that difference can significantly affect final corpus.

Long-Term Insight

Even a 0.75% annual cost difference can translate into substantial wealth variation over long investment horizons due to compounding.

NAV Difference Between Direct and Regular

Since expenses are deducted before NAV is declared, Direct plans typically show slightly higher NAV compared to Regular plans of the same scheme.

This does not mean Direct plans perform “better” in terms of portfolio selection. It simply means lower expenses allow more of the gross return to remain with the investor.

The portfolios are identical. The cost structure is not.

Over time, NAV charts of Direct plans gradually diverge upward relative to Regular plans.

Does Regular Plan Mean Bad?

Not necessarily.

Regular plans may provide value when:

An investor needs professional guidance.

An advisor assists in asset allocation and behavioural discipline.

Financial planning support is required.

Investors lack confidence in making independent decisions.

In such cases, commission paid may be justified if it adds advisory value.

However, investors should be aware of what they are paying for.

Hidden Cost Awareness

Many investors are unaware they are invested in Regular plans. Always verify plan type before investing.

When Direct Plan Makes Sense

Direct plans are generally suitable for:

Investors comfortable selecting funds independently.

Individuals following structured long-term strategies.

Those who understand asset allocation principles.

Cost-conscious long-term investors.

For disciplined investors, lower expense ratio improves compounding efficiency.

Behavioural Consideration

Financial decisions are not purely mathematical.

Some investors benefit from an advisor’s presence, especially during volatile markets. Panic selling can destroy far more wealth than a slightly higher expense ratio.

Therefore, the decision between Direct and Regular should consider not only cost but also behavioural discipline.

Regulatory Transparency

SEBI mandates clear disclosure of expense ratios and plan types.

Fund houses publish:

Separate NAV for Direct and Regular plans.

Separate expense ratios.

Portfolio holdings (identical across plans).

This transparency allows informed comparison.

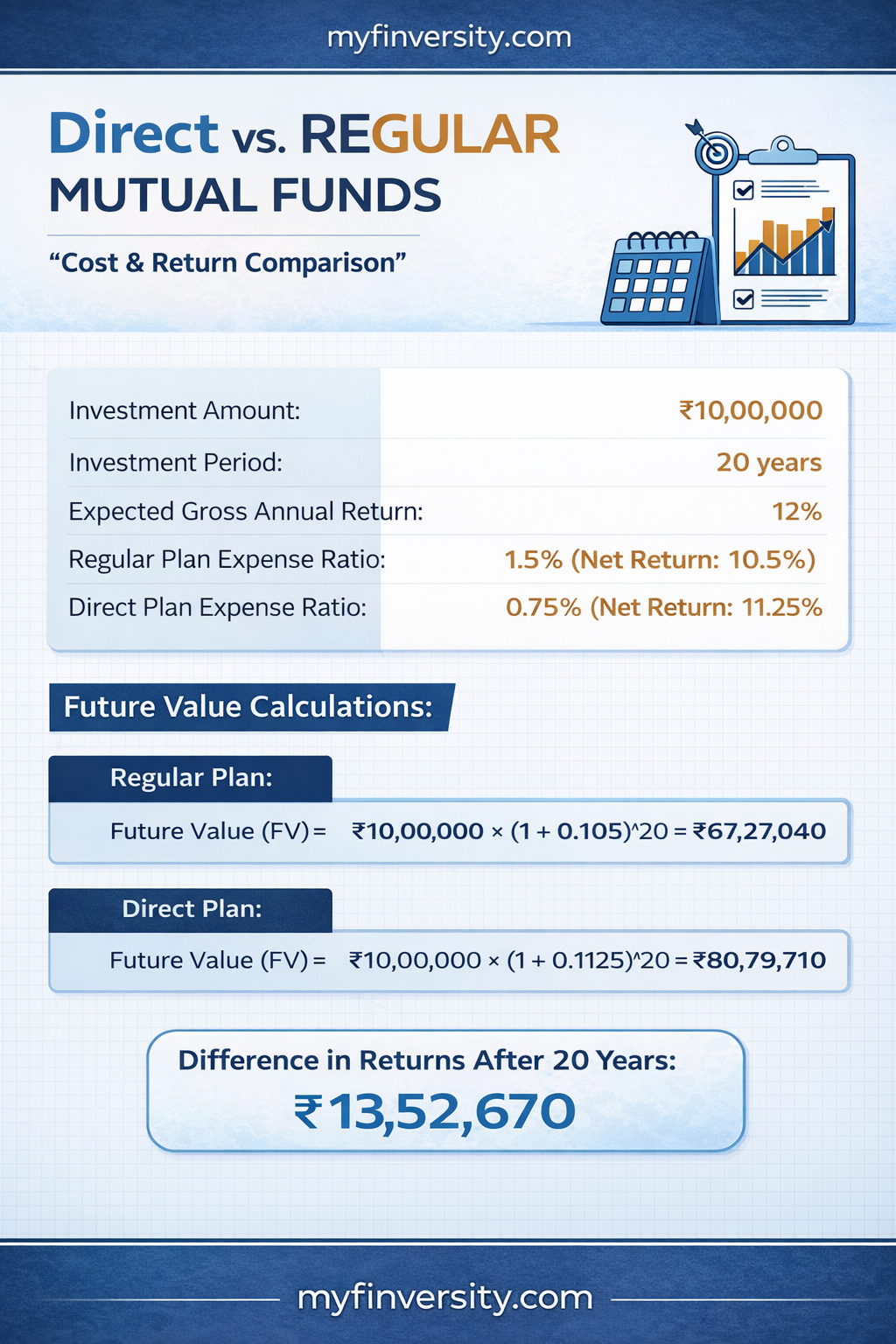

Illustrative Impact Over Time

Assume:

Investment: ₹10 lakh

Return before expenses: 12% annually

Investment duration: 20 years

If Direct plan net return: 11%

If Regular plan net return: 10%

The difference in final corpus can run into several lakhs — purely due to cost differential.

Cost efficiency compounds just like returns.

Final Perspective

Direct and Regular plans invest in the same portfolio. The difference lies in cost and distribution.

Direct Plan: Lower cost, self-directed investing.

Regular Plan: Higher cost, distributor involvement.

There is no universally “correct” choice. The correct choice depends on the investor’s need for advisory support versus cost sensitivity.

What matters most is informed selection — not accidental allocation.